- Liittynyt

- 17.10.2016

- Viestejä

- 17 527

Kiitos vastauksista tuohon todella nyyppätason kysymykseen.Oletin, että verot maksetaan siihen maahan, minkä pörssin osakkeilla tehty kauppaa, eli tässä tapauksessa Jenkkilään ja myyntivoittovero tilitettäisiin sinne heti tai viimeistään vuoden lopussa. Huomaa varmasti, etten todellakaan ole vielä juuri tehnyt kauppaa ulkomaisilla osakkeilla.

Lähdemaahan maksetaan kyllä muita veroja. Esim. osingoista maksetaan useaan maahan lähdevero heti maksettaessa. Ihan riippumatta onko osakkeet OST:llä tai AOT:llä. Sen suuruus vaihtelee mutta 15% on aika yleinen. Tuohon sitten liittyy erilainen verokohtelu Suomen verotuksessa riippuen oliko OST tai AOT.

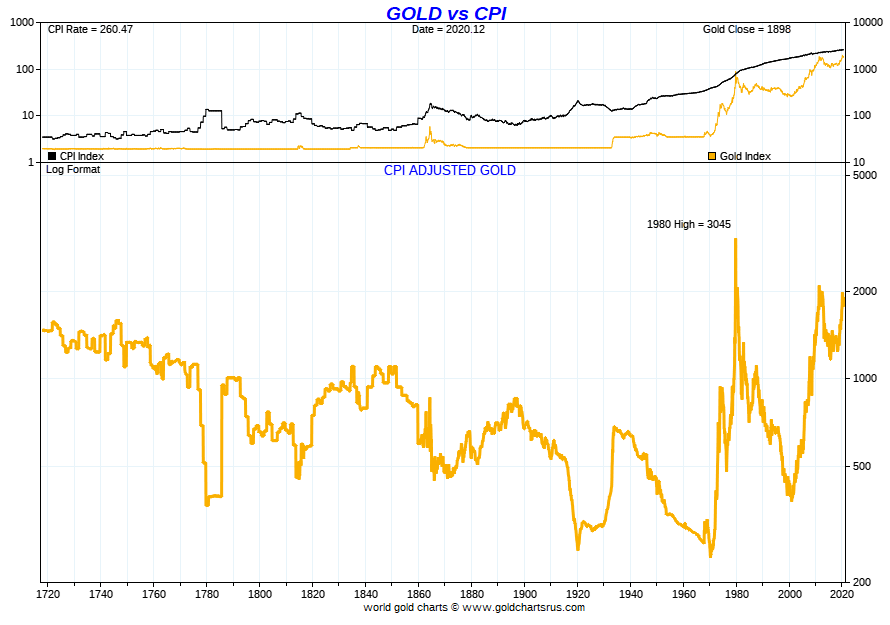

") Kulta lienee suhteellisen hankala vaihdon väline käytännössä jos tulee oikein huono tilanne ja käteisraha menettää arvonsa. Jos menet kauppaan kilon harkon kanssa josta kassa vuolee lastuja maksua varten niin tuskin montakaan kauppareissua tarvitsee tehdä ennen kuin joku isompi ja ilkeämpi ottaa sen harkon. Gramman, parin kolikot/harkot on taas suhteessa kalliita hankkia eikä kaikilla ole välineitä tehdä sellaisia itse kun tilanne tulee päälle.

Kulta lienee suhteellisen hankala vaihdon väline käytännössä jos tulee oikein huono tilanne ja käteisraha menettää arvonsa. Jos menet kauppaan kilon harkon kanssa josta kassa vuolee lastuja maksua varten niin tuskin montakaan kauppareissua tarvitsee tehdä ennen kuin joku isompi ja ilkeämpi ottaa sen harkon. Gramman, parin kolikot/harkot on taas suhteessa kalliita hankkia eikä kaikilla ole välineitä tehdä sellaisia itse kun tilanne tulee päälle.

Suurimmalle osalle ja ehkei pitkässä juoksussa allekirjoittaneellekaan tosiaan tällainen kikkailu kannata, kun ei huippuammattilaisetkaan siinä keskimäärin onnistu. Siksi ei pitäisi antaa rommailun pelon vaikuttaa koskaan omaan sijoitussuunnitelmaan.

Suurimmalle osalle ja ehkei pitkässä juoksussa allekirjoittaneellekaan tosiaan tällainen kikkailu kannata, kun ei huippuammattilaisetkaan siinä keskimäärin onnistu. Siksi ei pitäisi antaa rommailun pelon vaikuttaa koskaan omaan sijoitussuunnitelmaan.